Wealth Building 101 (Part 2)

Stocks and Bonds and Risk…Oh My!

“It’s possible to have risk (a good thing) without debilitating fear or its best friend, obsessive worry.” ~~Seth Godin

In our last post, we reviewed the first 4 lessons of Wealth Building (Read Part 1). The 5th one brings us to one of my favorite subjects—risk, a word that, when used in the same sentence as money, used to scare me silly.

Wealth Building Lesson 5

Webster’s definition of risk is: the possibility of suffering harm or loss. That’s how I always regarded investing—as a guarantee of losing all my money. But when I interviewed women who were smart about money, they had a vastly different take on risk.

To them, risk provided the opportunity for gain.

This is worth repeating:

Risk provides the opportunity for gain.

In the market, risk is linked to volatility. Prices go up; prices go down. But price swings only matter when you sell. Everything else is just noise—the sound of the markets doing what markets are supposed to do: up/down/up/down/up/down.

Because we’re talking about investing for the long term, we need to discipline ourselves to turn a deaf ear to erratic markets.

So, let’s talk about a couple of ways to minimize your risk of loss and maximize your gains. Here’s the first:

Wealth Building Lesson 6

One way to diminish risk is by understanding how “Time” (not “Timing”) works. Markets function like roller coasters. They go up; they go down. All investments go down on occasion. Some do so more frequently and severely than others, but even the best will go down at times.

Here’s what to remember. Market gyrations only matter when you sell your holdings. It’s called the Rule of the Roller Coaster (borrowed from the late Paul Harvey):

The only one who gets hurt riding a roller coaster is the one who jumps off.

When people try to time the market—buying when they think it’s going higher and selling when they’re sure it’s about to go down—that’s not investing; that’s gambling. Here’s the big secret to stacking the odds in your favor:

Respect the time factor.

Here’s what I mean by that:

Money you’ll need in 1-3 years—CASH

Money you’ll need in 3-10 years—STOCKS, BONDS, & CASH

Money you’ll need in 10+ years—STOCKS, REAL ESTATE & COMMODITIES

If you don’t know when you’ll need the money, err on the safe side. Invest your cash in liquid assets like cash, stocks or bonds that are easy to sell.

Wealth Building Lesson 7

I call this lesson the First Law of Investing. It’s short but not always simple.

Never invest in anything you don’t understand.

If you don’t understand what you’re buying, you won’t be able to properly evaluate information to know when to sell.

Wealth Building Lesson 8

Perhaps the best way to minimize risk of loss when investing is through diversification. In other words, don’t put all your eggs (money) in one basket. Remember we talked about the five asset classes in my last post (Wealth Building 101 Part 1). Each of the asset classes is a different basket: stocks, bonds, real estate, cash, and commodities.

If you have your portfolio diversified, some of the baskets will be going up while others may be going down. Diversification protects your overall holdings. In fact studies show that diversification accounts for 93 percent of a portfolio’s overall performance. 2 percent comes from stock picking and 3 percent from luck.

Only 2 percent from picking the right stock. Instead of making ourselves crazy trying to find the best companies, we should be putting our energy into making sure we’re sensibly spread out over numerous categories.

Wealth Building Lesson 9

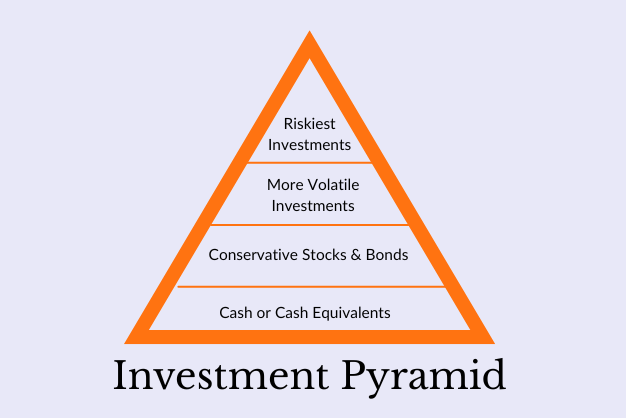

When I first learned about the Investment Pyramid it was like a huge lightbulb went on in my head.

In my first excursion back into the market after selling everything in the 1987 October crash, I purchased a limited partnership in T. J. Cinnamons, a company that sold sticky buns in shopping centers. My first big mistake was investing in something I didn’t understand. Oh, I knew what a sticky bun was, but I knew nothing about limited partnerships. Because my father’s friend who was smart, successful, and wealthy entrepreneur, I trusted him completely and gave him some money. I did not realize that a limited partnership is totally illiquid. When the company went bust, I lost everything because I couldn’t sell my shares.

Fortunately, my investment was small enough that it didn’t wipe me out. Later, I was sharing my tale of woe with my CPA, when he whipped out a piece of paper and drew a triangle on it. He explained that the best investment strategy is based on the traditional upright pyramid. My mistake was that I’d started with the risky investments that should have been at the top of the pyramid

. “See what happens when you start at the top? He explained. “Your portfolio is not very stable, is it?” Suddenly the whole topic of investing made sense. Here’s a brief list of the levels:

Level 1: Cash or cash equivalents. This is your “Sleep at Night Money”. There’s little volatility at this level. This level includes CDs, treasuries, money market funds, and basic bank accounts.

Level 2: Conservative stocks and bonds. This is your “Inflation-Fighting Money.” At least a portion of your portfolio needs to grow faster than inflation. Level 2 can include big, solid companies, higher-rated bonds and mutual funds with a good track record. These investments are still very liquid so they can easily be converted to cash if needed.

Level 3: More volatile investments. These are “Pack a Punch” investments. They include emerging markets, foreign funds, and junk bonds. Price swings can be unrelenting and extreme, but these investments can ratchet up your returns significantly.

Level 4: Riskiest investments. I affectionately call these the “Wild Ones.” They include limited partnerships, venture capital, hedge funds, derivatives, options, and commodities. Gains here can be enormous but so can the losses. I rarely invest here, because, frankly, I don’t understand most of what’s offered.

I’ll wrap up these Wealth Building Lessons in my next post with a few more tips and a three-step formula for financial success.

What if the breakthrough you’re looking for isn’t about doing more?

What if it’s about understanding, at a deeper level, how you actually create your reality?

After nine years, I’m bringing Sacred Success back with an entirely new framework that blends Spirituality, Psychology, Neuroscience, and Quantum Physics into a practical path for creating greater wealth, purpose, power, and possibility.

If you’ve been sensing that you’re meant for something bigger, this retreat will help you understand the forces that shape your reality—and how to work with them rather than against them.

Sacred Success: The Next Evolution

October 22–25, 2026

Silver Cloud Hotel at Point Ruston Waterfront, WA State

Early Registration is now open.

Risk is something I’m leaning into more too, especially after I heard that a freeze response in our nervous system can occur when choosing between being a “good girl” or a “risky one”.